Paul Kennedy, in his 1987 book The Rise and Fall of the Great Powers, forecast that Japan would continue to outperform the U.S. and Europe economically through greater exploitation of technology, while freeriding on the U.S. defence budget. In February 1988, the New York Times reported that international investors had jumped back into the Tokyo stock market. Strategists were no doubt arguing for a great rotation out of U.S. and European stocks into Japan based on this narrative.

A more recent narrative from strategists is for a great rotation out of bonds into equities. This story notes that yields are unlikely to fall much further and any small increase in inflation expectations will drive up yields causing capital losses for investors.

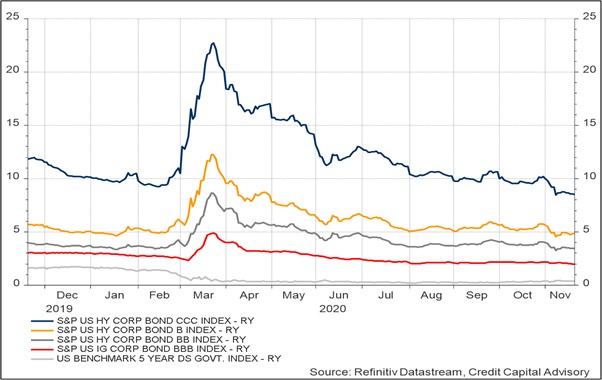

With average dividend yields higher than government bond yields, there is even less reason to hold bonds. Furthermore, last month the IMF forecast global GDP growth to fall by 4.4% in 2020, with advanced economies expecting a 5.8% fall. As a consequence U.S. default rates are expected to rise to levels not seen since the financial crisis to around 12% from its current level of 6%.

Despite this potential shock to investors, U.S. bond spreads – even for the CCC rating category – have returned to pre-pandemic levels. The market, it appears, expects the Fed to keep on buying corporate bonds depressing spreads further, thereby generating higher returns.

Moreover, the inflation picture remains subdued with five year forward expectations below 2%, although the market is expecting inflation to head up towards 1.5% in November, based on the difference between the five year TIPS spread and the nominal benchmark.

Chart 1: U.S. Bond Market Indicators

The reality is that our ability to understand the potential trajectory of complex systems is inherently limited, hence stories explaining the next big investment idea should always be treated with suspicion. While there is often a grain of truth in these narratives, other variables that tend to be ignored at the time often become more important, rendering such narratives redundant. In the case of Japan, it was unsustainable levels of private debt which resulted in equity values falling by more than 50% between 1990 and 1992.

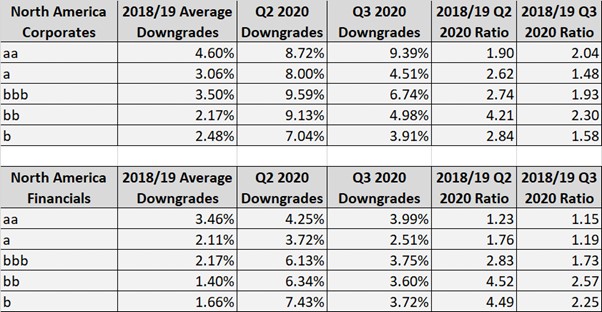

In terms of bond market performance, defaults as noted can be expected to jump, but these take time to filter through the economy. The latest transition matrices from Credit Benchmark show a continued downward transition of obligor ratings, indicating speculative bond investors are indeed overly exposed.

While the Q2 downward transitions were dramatic, the Q3 transitions suggest an element of stabilization, particularly in the lower credit categories. To a certain extent, this is positive news as it indicates that an already difficult situation is not deteriorating further. However, this does not reduce the reality that defaults will still rise, resulting in losses to investors.

Table 1: Credit Benchmark Credit Transition Matrices

Source: Credit Benchmark

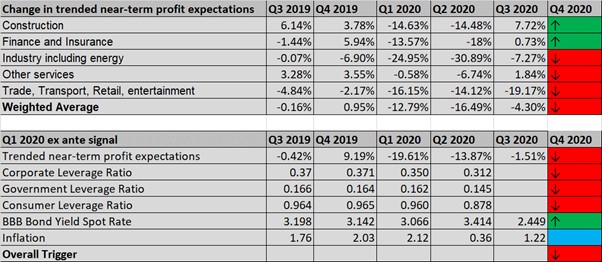

While the future for bond investors doesn’t appear particularly bright, the assumption that what is potentially negative for bonds is necessarily good for equities does not always follow. Near-term profit expectations for the U.S. economy indicate a negative outlook for profit growth and yet the S&P 500 is at record highs.

While recent arguments for a great rotation out of tech stocks into the rest of the economy have been made, such a view is difficult to substantiate given that firms’ rate of profit growth is falling, not rising, thereby making it much harder to sustain rising capital values.

Table 2: Near term profit outlook for U.S. equity market

Source: Refinitiv, Credit Capital Advisory

This raises the question of whether bond investors will get caught out with a jump in yields or whether overvalued equity markets might fall, thereby placing a greater emphasis on the return of capital rather than a return on capital.

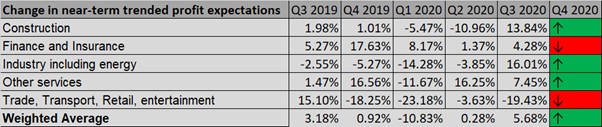

As was noted in last quarter’s note, near term profit expectations are rising in China, indicating that capital values are more likely to rise. While tensions between the U.S. and China are unlikely to recede under the new U.S. administration, there is little evidence of a complete economic decoupling. This positive profit outlook for China is set to continue, although firms providing consumption goods and services remain in a difficult position.

Table 3: Near term profit outlook for China equity market

Source: Refinitiv, Credit Capital Advisory

This strategy since September would have rewarded investors, with Shanghai outperforming Nasdaq by 3%, although this was trumped by the Japanese stock market which beat Nasdaq by 9%. This is why some investors are beginning to wonder whether this time might really be different for Japan. Although short term profit expectations are improving, which will likely improve the capital value outlook, they are not yet in positive territory.

Table 4: Near term profit outlook for Japan equity market

Source: Refinitiv, Credit Capital Advisory

While stories may help investors understand what is driving capital values, they can also act as a confirmation bias leading to potential losses, as investors discovered in Japan in the early 1990s. Assessing near term profit expectations and leverage ratios may not generate great stories, but it does help reduce risk by avoiding exposure in asset classes that are not justified by rising profit expectations or lower default rates.

Credit cycle investing has year to date generated returns of 40%. In the first two months of the year, declining U.S. profits indicated an asset allocation for bonds, which switched into U.S. tech in March despite the pandemic, and then into China equities in August.

Chart 2: Year to date returns on assets

The trajectory of complex systems cannot be explained by simple stories, which is why narratives of great rotations ought to be rejected. One way of avoiding market narratives is to invest across the credit cycle based on near term profit expectations and leverage ratios. This approach provides greater insight into the changing dynamics of complex systems, and also happens to be a reasonably profitable one.