On March 1, the Dow plowed through the 21,000 barrier. Many market commentators sought to attribute this rise to President Trump’s congressional address the day before. Given that there was little policy detail in the speech, there seemed to be general agreement across the market that it was the tone of the speech that did it.

It is certainly plausible that the tone of a newsmaker’s speech might send the market up or down. It is, however, much harder to ascertain the exact reason why the aggregate output of several billion shares changing hands in a day is due to a single driver.

The economy is a much more complex system than many financial market analysts would have us believe. When investors see headlines about a jobs report change in the space of 30 minutes from “stocks rise on jobs report” to “stocks fall on jobs report” before changing it to “stocks fluctuate on jobs report,” it should be a wake-up call! Investors buy and sell shares for a variety of different reasons, many of which are quite mundane. Thus, attempts to simplify the economy should just be ignored.

Investors need to focus on what is knowable. When it comes to equity markets, that includes short term profit expectations and changing patterns of leverage that respond to changes in profit expectations. Using this neo-Wicksellian model it is possible to discern the short-term profit outlook and generate above average returns with lower volatility.

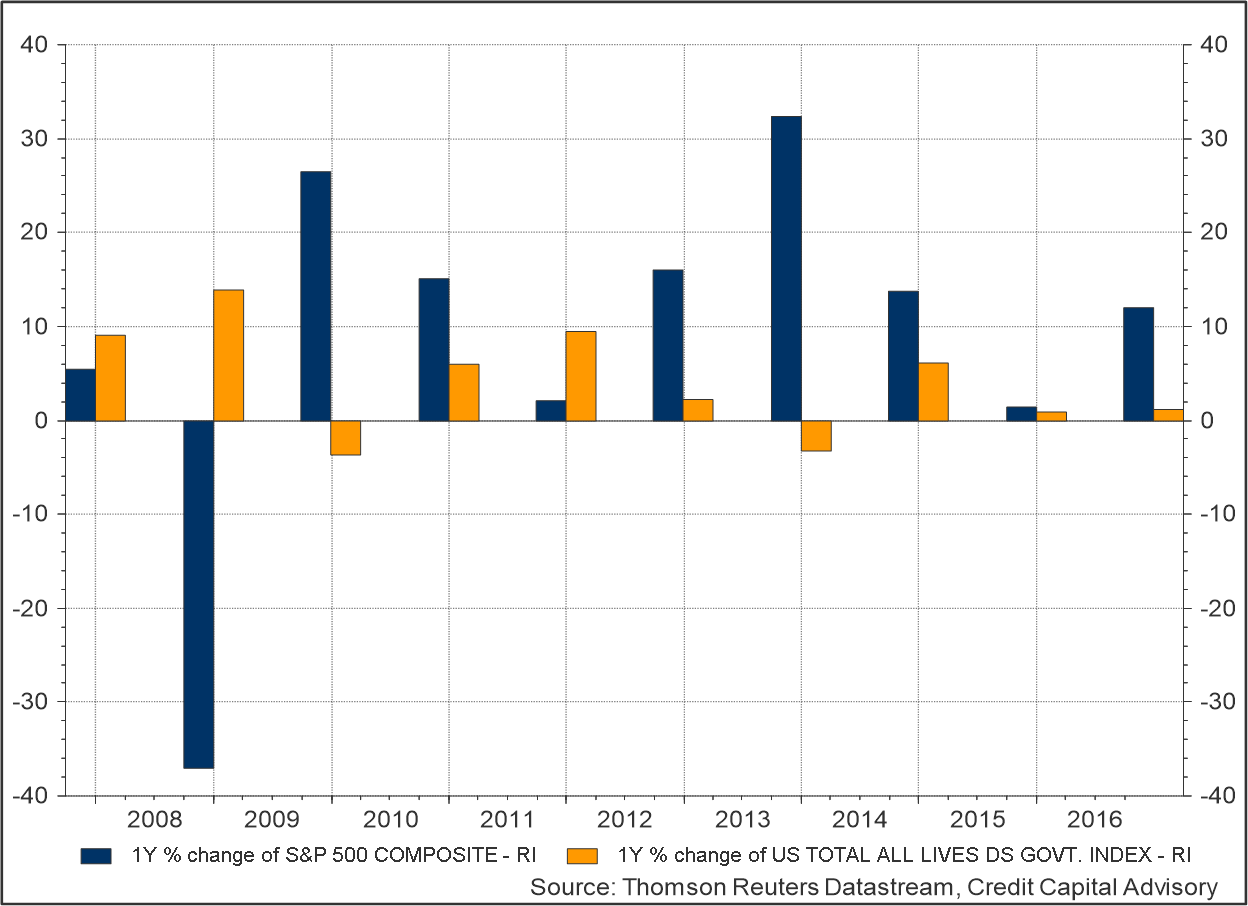

Chart 1 shows the annualized nominal returns of U.S. government bonds and equities since 2007. The capital destruction of 2008 highlights why asset allocation matters. Using a neo-Wicksellian strategy doesn’t get the top performing asset class right every year, but it has a track record of avoiding the downside thereby outperforming both bonds and equities with lower volatility.

Exhibit 1: Comparison of U.S. government bond and equity returns 2007 – 2016

Profit outlook changes

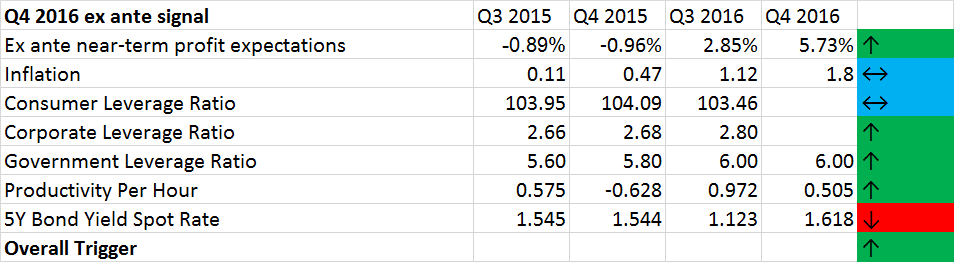

Coming into 2016, profit expectations were still negative, implying investors should have been in bonds. However, by the time Q3 earnings were out in October, profit expectations had become positive implying a stronger outlook for equities. This trend was further amplified by the Q4 earnings reports.

Although not all sectors since Q3 have seen rising profit expectations with the construction sector along with trade, transport and retail lagging, the overall weighting across sectors is positive. In addition, to the positive near term profit expectations signal, there has been a major jump in the corporate leverage ratio along with productivity. This is why the signal has been positive for equities since Q3 earnings results.

Exhibit 2: Credit cycle indicators

Source: Thomson Reuters Datastream, Credit Capital Advisory

Sector rotation

The gentle rise of bond yields may have also supported equity valuations in the last few months as part of a broader rotation out of bonds into equities. It is also possible that the cause of rising bond yields has been the tone of President Trump’s announcements. However, the fact that inflation is now running at 2.5%, with the Fed expected to raise short term rates, may be a more plausible explanation.

Investors who chose to follow a post truth approach to investing and take bets on the tone of President Trump’s utterings may end up generating good returns. Then again, it might not quite work out as expected. Investors might be better off paying more attention to what is actually known and adjusting to new information as it become available. A combination of company profit expectations, the propensity for leverage and a handful of macro factors are all that is needed to generate above average returns through the cycle.