The Reserve Bank of India cut the policy repo rate by another 0.25% on June 2 to 7.25%. The market reaction sent the SENSEX index of Indian equities down by 660 points – nearly two and a half per cent. Bank governor Raghuram Rajan commented that he remained concerned that below-normal monsoon rains, global crude oil prices and external risks all pose a threat to inflation. The market appears to have interpreted these comments as indicating the end of the downward movement in interest rates, hence the sell-off.

However, when the monsoon rains kicked in during the week of June 15, they were better than forecast. The possibility of an interest rate rise to curtail potential rising inflation expectations due to higher food prices has now fallen. As a result the SENSEX surged more than 3% during that week.

The fact is, India has an inflation problem that needs to be tackled. But utilising the monetary policy status quo of an inflation target is not a good solution. The cost of capital should be influenced by what is happening in the real economy and not whether it rains.

India’s inflation challenges, particularly related to food, are more supply side related and would be better resolved through further reform by Prime Minister Narendra Modi’s administration in conjunction with a nominal income target. Jacking up interest rates every time the monsoon disappoints, particularly when by most measures Indian monetary policy remains far too tight, is a bad idea. Such an approach will only lead to more capital destruction, with higher levels of non-performing loans and businesses defaulting.

Down, down, inflation and down

Earlier this year, the government and the central bank agreed to set a consumer inflation target of 4% with a band of plus or minus 2% from the financial year ending in March 2017. The governor of the central bank is now trying to drive down longer term expectations and anchor inflation to much lower levels. This focus on inflation is to be welcomed given India’s history with rising prices compared to many other large emerging economies.

The reasons behind India’s inflation challenges are multifarious, including a high degree of dependence on crude oil imports for energy, the uncertain impact of the monsoon rains on food production and poor infrastructure negatively impacting the distribution of goods across the country. But things are clearly improving. As chart 1 shows, inflation is now at its lowest level since the financial crisis.

Although inflation has reached its lowest levels in years, inflation expectations ticked up in the last expectations survey , and annualized growth is now trending at 7.5% higher than in China. These data points may have influenced Rajan’s caution on inflation. The repo rate is at similar levels to 2013 when inflation was almost double that of today.

Chart 1: Inflation, GDP growth and nominal interest rates in India

Inflation targeting all over the world

From a monetary policy perspective, the history of inflation targeting appears to have been remarkably successful. Since the early 1990s, when central banks began to target inflation, it has fallen substantially. However, as Greg Mankiw has pointed out, inflation also fell in those countries where there was no inflation targeting — implying that there are other causal factors at work driving down inflation. In particular, the addition of hundreds of millions of workers from China and India that entered the global supply chain has been a significant disinflationary factor.

A number of criticisms of inflation targeting have also arisen in recent years. First, William White at the Bank for International Settlements (BIS) raised concerns that price stability on its own could not provide financial stability as credit growth boomed without generating inflation. This highlights the flaw in Irving Fisher’s highly influential theory that the over-heating of an economy would reveal itself in rising inflation. Fisher’s theory assumed that excess liquidity would be ploughed into the real economy. But as the run up to the financial crisis demonstrated, excess liquidity can also flow into existing assets such as housing causing significant macroeconomic instability.

Second,, concerns have been raised in emerging market economies that inflation targeting could be damaging to economic stability, particularly if the reasons for inflation were commodity driven. Both the central banks of Chile and South Africa have highlighted these issues related to imported oil and food prices. For example, inflation in Chile reached 9.9% in 2008 mainly due to rising commodity prices, and these rises also drive up inflation expectations. Central banks pursuing an inflation target would therefore be required to raise interest rates to quash rising inflation expectations. But such a rise in rates would reduce nominal income, leading to a slowdown in the economy.

The same is true for India today. If poor monsoon rains and rising oil prices feed through into inflation expectations, then the Reserve Bank of India might need to start raising rates given its new mandate. However such a move would reduce nominal income growth leading to a sub optimal outcome. Furthermore, any rise in interest rates at this stage would be counter to other indicators that demonstrate India is operating significantly below its potential.

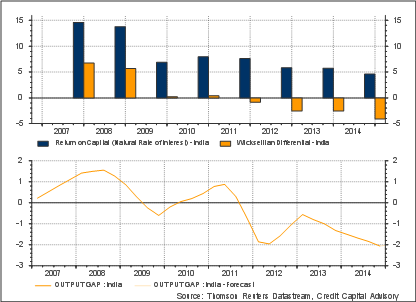

Output gap measures show India remains 2% below its potential, with the economy not expected to be at equilibrium until 2025. Although output gap estimates are notoriously unreliable, other indicators such as the Wicksellian Differential derived from credit disequilibrium models also show that the economy remains significantly below its equilibrium level. Indeed, the Wicksellian Differential – the difference between the return on capital and the cost of capital – shows that monetary policy in India is still causing capital destruction.

Chart 2: India: Return on Capital v Wicksellian Differential and Output Gap

This highlights two issues. First, a form of nominal income targeting would be a far more effective way of managing exogenous price shocks that constantly arise. Second, and perhaps more important, is that governments in most countries continue to abdicate their responsibilities to reform the economy by assuming that monetary policy can resolve every economic issue. Monetary policy can achieve a lot, but it cannot resolve everything. Even if India had a nominal income target whereby interest rates didn’t automatically rise with commodity price inflation, the lack of focus on supply side policies to drive productivity growth would mean India’s economy would continue to fall short of its potential.

Whatever you want, as long as it’s not supply side reform

Over the last four years, the three categories of inflation in India that have grown faster than the CPI are housing, clothing and food. Wages have stagnated at around the 3% growth level, with most other goods and services rising at lower rates than the CPI. The recent fall in the CPI has been largely due to the fall in the price of oil, as just under a third of India’s energy is derived from oil. This high level of dependence on volatile external oil prices is clearly a major macroeconomic issue. Plans are afoot to build more renewable and nuclear energy power sources, but to date this remains a fraction of India’s power generation capability.

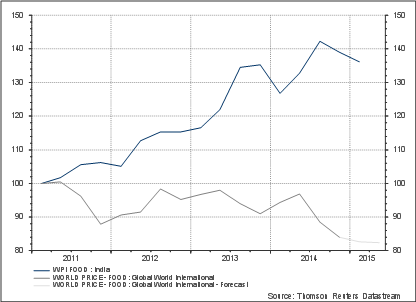

When it comes to food, the data in chart 3 is striking, which shows that as global food prices have fallen, India’s food prices have risen. Food prices in India are sensitive to the monsoon rains because its agriculture has not seen the productivity growth it needs. The proliferation of small land holdings that don’t have the scale to use new technology has been a major barrier. India’s agricultural sector also remains highly protected from international trade. India subsidises food to the tune of $20 billion a year, just over 1% of GDP with the food security law introduced in 2013 offering minimum prices to farmers.

Chart 3: Food prices: India vs World

The reality is that food policy is highly politicized and the reduction in subsidies may lead to a loss of votes. Hence from a politician’s viewpoint, it’s much easier to delegate these kinds of problems to a central bank with an inflation target. But there is a major economic cost associated with this decision: excessively high interest rates and capital destruction.

Final fling

If the monsoon ends up as disappointing and food prices increase, a rise in interest rates would be highly damaging to the Indian economy. Although India does need to get on top of its inflation problem, pursuing an inflation target is not the best solution. A better approach would be to have some form of nominal income target in conjunction with a significant push by Modi on supply side reforms to mitigate price rises from commodity-driven inflation.