The central thesis of Piketty in his book is that when the return on capital defined by r grows faster than growth in income g, the net result is rising inequality. Those with capital therefore get richer than those without capital, leading to a society where meritocracy is replaced by a plutocracy. Some commentators have argued that the idea that capital begets capital does not fit the facts. Larry Summers in his review highlighted that the Forbes 500 list is very different today than it was 30 years ago. The fact that you were very rich does not mean that you will always be very rich.

This article will focus on demographics and pension liabilities and argue that Piketty is wrong to imply that r being greater than g is necessarily a problem. Indeed, if r does not grow faster than g, then the issue of pensioner poverty may well become the major social issue for the next generation.

Slowing population growth

Piketty highlights in numerous places that countries with higher birth rates have higher growth rates. Piketty particularly likes the “30 glorious years” when European countries saw higher birth rates and higher rates of growth leading to the returns to labour growing at the expense of capital. Piketty also recognises that most advanced industrial economies are seeing a marked slowdown in their birth rates, which is why he is quite pessimistic about the future level of growth.

When a society’s birth rate begins to slow down it has a major impact in one area of public policy: pensions. Most of the world’s pension systems are funded through the taxation of the working population, which is a good system when life expectancy beyond retirement is short and the rate of young people entering the workforce is increasing. This was the case when Bismarck set up the world’s first universal pension system in Germany in the 1880s. Fortunately and unfortunately for society, the conditions of the 1880s and 2014 are rather different. Average life expectancy has almost doubled during this period and the rate of population growth in most developed economies has declined below its replacement rate, which means that fewer and fewer workers are supporting an ever-increasing number of pensioners. This has led to a massive increase in future pension liabilities that working populations are not going to be able to fund unless there are massive cuts to virtually all other public services or a different approach to funding pensions is taken.

In response to this issue two things have happened. Firstly, in most countries the retirement age is rising as people are living longer – with the exception of France which decided to lower it. The second policy has been the realisation that the general growth of taxation will be insufficient to pay for these liabilities, leading to policies to support pension plans where individuals save regular amounts which are then invested in financial assets.

Hence the future expected rate of r will be closely linked to the success of public policy for pensions. Indeed, if r does not grow faster than g then either there will be a jump in pensioner poverty or substantial cuts in other public services such as health and education to alleviate these conditions. As a result advanced industrial economies with ageing societies require r to grow faster than g in order sustain themselves.

The problem with PAYG

Piketty’s response to this is curious. He argues that pay as you go pensions (PAYG) should remain which is where pension liabilities are paid out of general taxation. However he does not go into any detail as to how this could ever be sustainable given the demographics in advanced industrial economies. Another criticism he makes of funded pension plans, where the pension pot is determined by the amount saved and the investment return, is that the returns can be volatile. This is clearly true, however sensible asset allocation can avoid most of these issues. The fact that asset allocation advice is poor in many instances is a very different issue.

Piketty also argues that any attempt to move away from a PAYG system means that an entire generation is left without money. This throw-away remark is not backed up by any evidence. Australia has made the most concerted effort to date to shift future pension liabilities on to individual savers and Australian pensioners are not currently in dire financial straits compared to other countries.

Most curious of all though is the fact that funded pensions can’t be passed on to the next generation, so the growth in r to fund pensions by definition cannot lead to increasing intergenerational inequality.

r > g

Given that r must rise more than g if our ageing societies are to sustain themselves, it is crucial to address Piketty’s objections in a bit more detail. I will only deal with two of them here. Firstly is his argument that rising levels of beta automatically lead to more inequality. One aspect that is missing from Piketty’s analysis is a more detailed understanding of the ownership of financial assets. The rise of funded pension systems that invest in financial assets has led to a far greater democratisation of the ownership of those assets compared to 100 years ago. This is not to dispute that massive inequality still exists but that rising beta isn’t necessarily the cause of it.

The second issue raised by Piketty is that richer people can afford better advice and therefore become even richer. He cites sovereign wealth funds and university endowment funds who can afford investment “superstars” to drive incremental returns. The problem here is that there is about three decades of compelling academic research that highlights the very low probability of any fund manager being able to consistently beat the market in the medium term. Crucially it is very difficult to know ex-ante who these fund managers are going to be. For example, the fund that manages the money which generates income for the Nobel Prizes, including that for economics, has generated such poor returns that for the first time since the 1940s it will be reducing the cash value awarded to its recipients.

However, Piketty is right that the Harvard and Yale university endowment funds have produced better than average returns. One significant characteristic of their success has been their active approach to asset allocation. Asset allocation has long been considered the most important driver of returns, however too much of the fund management sector is focussed on trying to beat standard benchmarks through stock picking, and until this changes there will remain inequality in returns.

Pension funds need to be investing in low cost asset allocation funds that can invest through the business cycle providing equity like returns with bond like volatility. However there is not currently much choice in the market at competitive prices. One reason behind the lack of choice is that fund management companies’ business model is not performance-based. As long as managers can generate sufficiently robust cash flows from clients just by bringing assets on board and charging high fees then there is little incentive for the sector to provide useful products. Jack Bogle’s revolution at Vanguard has made significant inroads in to trying to change this, but there is still a long way to go. Secondly, the way the industry is regulated astonishingly does not require the sector to fully disclose all the costs they are incurring which of course are all passed on to investors as recently highlighted by Norma Cohen at the FT.

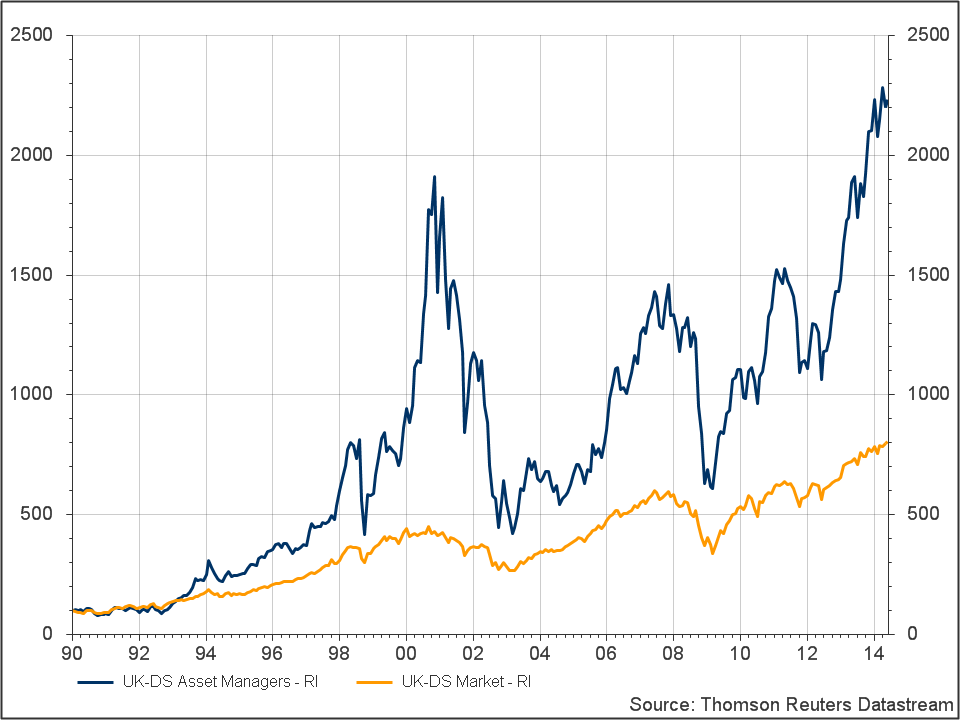

Hence there is in fact a significant issue with inequality, but it is between investors and the fund management sector. Chart 1 shows that the asset management sector has outperformed the broader market by nearly 3 times since 1990. It seems little has changed since William R Travers asked a friend of his in Newport Harbour in the 1880s “Where are the customer’s yachts?” This also became the title of a book by Fred Schwed published in 1940. The inequality between the returns to investors and the returns to fund managers is of supreme importance but alas none of this makes its way into Piketty’s tome.

Chart 1: Asset Management Sector vs UK Sector

In short Piketty’s gripe about r rising faster than g leading to rising inequality does not seem to fit with the general democratisation of asset ownership, and crucially the fact that faster rates of r can help solve the future pensions crisis and actually curtail inequality as pensions can’t be passed on to future generations. As such Piketty’s desire to see r grow at the rate of g ignores the key demographic issues he cites upfront in his book. A better approach to public policy would be to tackle the inequality between fund managers and their clients by forcing total transparency of all costs.